How Risk and Return create different terms and forms of funding for startups and growth companies

Was it ever difficult for you to understand the reason for unfavorable funding terms or for even being rejected by an investor? Or did you ever wonder why forms of funding are so fundamentally different? I hope this post can help to understand by explaining one of the most important principles of the investment business.

In the following, I will explain how risk and return are the fundamental principles of investing and how different terms and forms of funding emanate from this logic, e.g., venture capital, loans, venture debt, and revenue-based financing.[1] If you are not familiar with this topic, this might be an insightful read which could help understand the complex dynamics between entrepreneurs, investors, shareholders, and companies.

This post was originally written as background for my post on Non-Monetary Cost of Capital.[2]

Risk and return, a law of nature

All investment opportunities (i.e., companies) exhibit basic properties of risk and return. In this context, risk means the probability of not achieving the expected return on the investment or even losing money. The main driver of risk is inherent uncertainty about the outcome of an investment which will play a big role going forward.

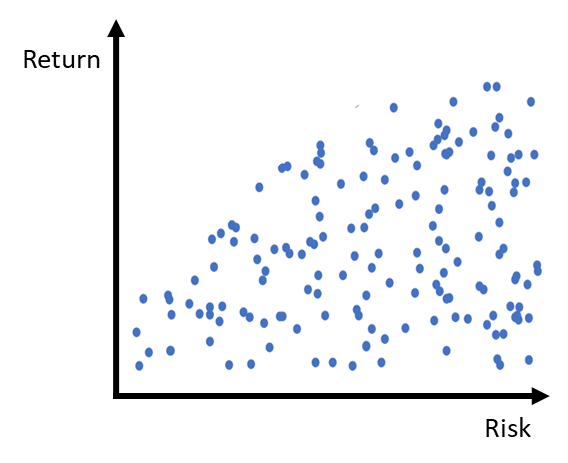

Hence, every company can be plotted in a risk/return graph as follows.

Note: Chart is for illustrative purposes only and does not reflect actual events.

The companies in this graph are distributed randomly across the spectrum because there are all kinds of different businesses out there. The upper left corner, however, is empty because for a given level of risk, return can’t be indefinitely high. But the lower right corner is not empty because for a given level of return, risk can be ‘infinitely’ high. To make an illustrative example, a company can be run by management “infinitely bad”, but you can’t have any infinitely high return potential for a given management team with its respective skill set. Such a company does not exit. Therefore, I call the upper left corner the Fairy Land of Risk/Return.

On the opposite side of the Fairy Land, the companies in the lower right corner bring too much risk for their return potential. This area is a No-Go Area for investors. It is populated by companies that do not get funding or should at least not get funding (from a macro-economic point of view, of course).

Hence, investors want to invest in a narrow band that stretches from the lower left to the upper right. Those companies have a reasonable ratio of risk and return: if you have low risk, low return seems appropriate; if you have high risk, you need high return (potential).

This is not my invention. This is one of the most basic principles of finance. Almost like a law of nature and a part of all great principles of finance. The most important implication is the notorious proverb that there is no such thing as a free lunch.

And by the way, not only should investors stay close to that optimal risk/return curve. Entrepreneurs should also make sure their business stays close to that curve to not waste time trying to realize a limited return with relatively high risk.

All forms of funding obey this law of nature

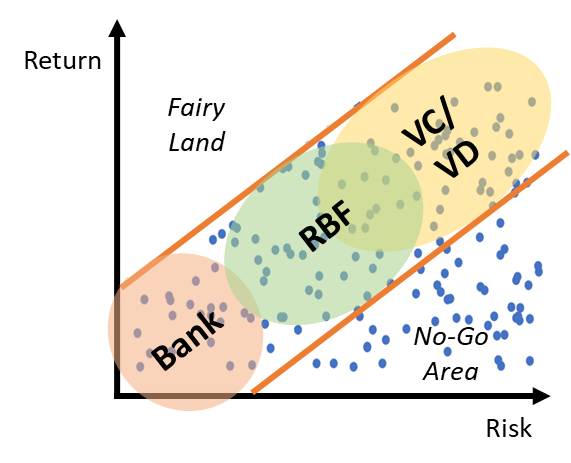

The important insight for us is now that investors position themselves within this band of optimal risk/return ratio, so that their individual financing instrument (i.e., VC/equity, loan, …) is a good fit for the respective position in this band. Or, to put it the other way around, each position in the band demands its individual form of funding to make it work.

The following graph and comments below make this more concrete.

Note: VD = Venture Debt; chart is for illustrative purposes only and does not reflect actual events.

Bank loans provide a fixed, moderate return through interest rates. Their return does not scale with the success of the company. That means banks can only accept very limited risk. Or to put it the other way around, since banks accept only very little risk, they can only demand a low return. Therefore, banks sit at the lower-left end of the risk/return band.

Venture capital buys a share of the entire company and its value which scales with the company’s success. It can cope with very high risk because it only invests in companies with very high potential return. Usually, it demands a return of at least 3x up to 10x of its investment. Of course, the return can also go down to zero. Therefore, venture capital sits at the top-right end of the risk/return band.

Venture debt (VD) comes in the form of simple term loans or in combination with options on equity (i.e., warrants). The latter is more common in my experience, so let’s focus on that. The combination of a term loan with a warrant (i.e., with the right to demand a share of the total value of the company, e.g., in case of an exit) means that venture debt uses a mixed calculation to make risk and return match. Venture debt only yields an attractive return for the investor if the warrant also delivers a return in the future. Therefore, the company must exit at an attractive valuation. And therefore, venture debt’s goals and investment criteria are in most cases the same as for venture capital investors. Both look for companies with a high return (but can also accept high risk). Hence, venture debt is not an alternative to venture capital but an add-on which works like a leverage on equity. Consequently, venture debt sits approximately in the same area in the graph as venture capital.

RBF sits between banks and venture capital but also covers a big part of the venture capital space. It can fund companies with less return potential than venture capital, but as well companies with higher risk than banks. It also works for risk levels associated with venture capital, but only up to a point because RBF has a capped return potential since it does not own equity (which also caps the cost of capital for investees). Therefore, RBF can be used as an alternative to venture capital (albeit with lower investment amounts in most cases), but it can also be used as a complement (i.e., in combination with venture capital).

Two insights to take away

The individual funding terms which a company might be offered by an investor are a reflection of the described principles. The higher the risk of an investment in the investor’s opinion, the less favorable the funding terms in the investee’s opinion (i.e., the lower the valuation in case of venture capital, or the higher the interest rate). Or the investor rejects the company altogether if she does not regard the company to be within the appropriate risk/return area.

The basic mechanics of the described forms of funding are not sufficient for an investor to find and hold a position on the optimal band within the risk/return distribution. In addition, investors will add properties to their funding instrument which either reduce risk or increase return. And those properties cause ‘non-monetary’ costs for founders and companies.

Now, I suggest you jump (back) into the post on Non-Monetary Cost of Capital.(b) Moreover, to get the full picture, you may also read my adjacent post on monetary Cost of Capital.(c)

Disclaimer: Christian Stein is an investor at Riverside Acceleration Capital. The content of this article reflects his personal views. The analyses and conclusions contained in this article include certain statements, assumptions, estimates, and projections that reflect anticipated results and have been included solely for illustrative and informational purposes and do not reflect actual events. This is not an offer or sale of, or a solicitation to any person to buy, any security or investment product or investment advice.

[1] A Primer on Revenue-Based Financing (RBF) via riverside.ac

[2] Start thinking about your Non-Monetary Cost of Capital via riverside.ac

[3] How growth companies and startups should think about Cost of Capital via riverside.ac

We love meeting new software companies, so let's talk.